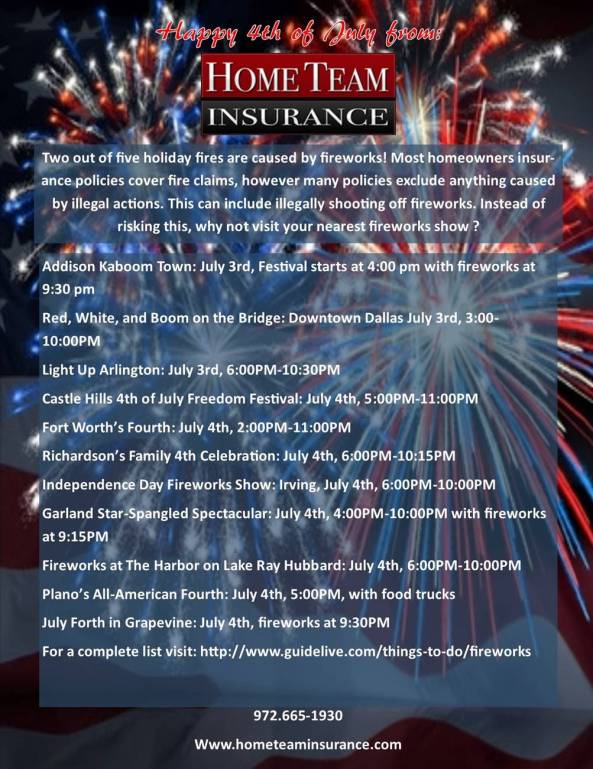

If you need insurance for Home, Auto, Life, Health or Commercial, just contact my trusted pal Nick Klein with Home Team Insurance!

Stay Safe & Happy 4th!

-Dawn Redmond – Your #1 Murphy Area Realtor

If you need insurance for Home, Auto, Life, Health or Commercial, just contact my trusted pal Nick Klein with Home Team Insurance!

Stay Safe & Happy 4th!

-Dawn Redmond – Your #1 Murphy Area Realtor

With an increasing population of seniors over the age of 62, otherwise known to most as the Baby Boomers, Texans took a great step forward in 2013 by voting into law the ability of seniors to purchase a home with a reverse mortgage. The term “reverse mortgage” can strike fear in the hearts of many that hear it, but it need not be so! Many – even seasoned real estate professionals – are confused at how reverse mortgages work, and the notion that one could purchase a home using such a tool is even more foreign. As odd as it may seem, this valuable program will be a tremendous opportunity for many Texas seniors.

Many seniors feel “trapped” in their current situation out of fear of not being able to qualify for a new mortgage and/or not being able to afford the mortgage payment on a new home. The most common reasons seniors list as to why they wish to move are that their home is too large/hard to care for, too far from relatives or other important medical/support services, or that they need a home with greatly reduced expenses. The reverse mortgage for purchase program offers tremendous hope and opportunity for these seniors to purchase the home of their dreams for their retirement years.

A down payment of 40-50% of the purchase price of the new home is required and there is no other income or credit qualifying for the senior (barring foreclosure and bankruptcy info that could preclude a borrower from obtaining a reverse mortgage for purchase like any other mortgage.) Like a reverse mortgage done as a refinance, there are never any payments due as long as at least one of the original borrowers on the loan live in the home. The predominant way that seniors who wish to use this program would obtain the necessary down payment is the sale of a current home that no longer fits their needs.

Out of all the fears listed as a reason why people don’t pursue reverse mortgages, the number one objection is “the bank will take the house” and that is simply not true. Like a traditional “forward” mortgage, there is a lien filed against the home by the bank, and just like any other mortgage, as long as the mortgage debt is satisfied per the terms of the mortgage, the bank never “owns” or “takes” anything. There is also never any recourse against a borrower/home owner’s estate for any debt incurred by the borrower on a reverse mortgage during their life. The estate can dispose of the home as they see fit (or directed in the will) in essentially an identical way had there been no reverse mortgage done at all.

Lastly, the reverse mortgage for purchase program is an FHA insured loan, which means this is not some clever gimmick that Wall Street created to fleece seniors with a scam of a mortgage product. In 1998 President Reagan signed the bill into law authorizing reverse mortgages and in 2008 Congress voted in the ability for the use of the program for the purchase of a home. There are significant consumer protection oversight check features built in.

With all of this being presented, is a reverse mortgage purchase right for every senior who wishes to buy the retirement home that best suits them? Absolutely not. But it will provide a sound and proven solution to home purchase for those that it fits and were otherwise unable to make any changes in their situation. Make sure anyone you know who is in this situation gets in contact with a trained, experienced mortgage professional to educate them on whether this is the right program for them.